If you’ve spent any time reading about retirement planning, you’ve probably come across something called the 4% rule.

Some people describe it as the simplest way to estimate how much you can safely spend each year in retirement.

Others argue it no longer works in today’s economy.

So who’s right?

The answer is somewhere in the middle.

The 4% rule is still one of the most widely discussed retirement guidelines, but it was never meant to be a guarantee. Like most financial rules of thumb, it works better as a starting point than a one-size-fits-all solution.

Let’s take a closer look at where the rule came from, why it became so popular, and whether it still makes sense for retirees today.

What Is the 4% Rule?

The basic idea is surprisingly simple.

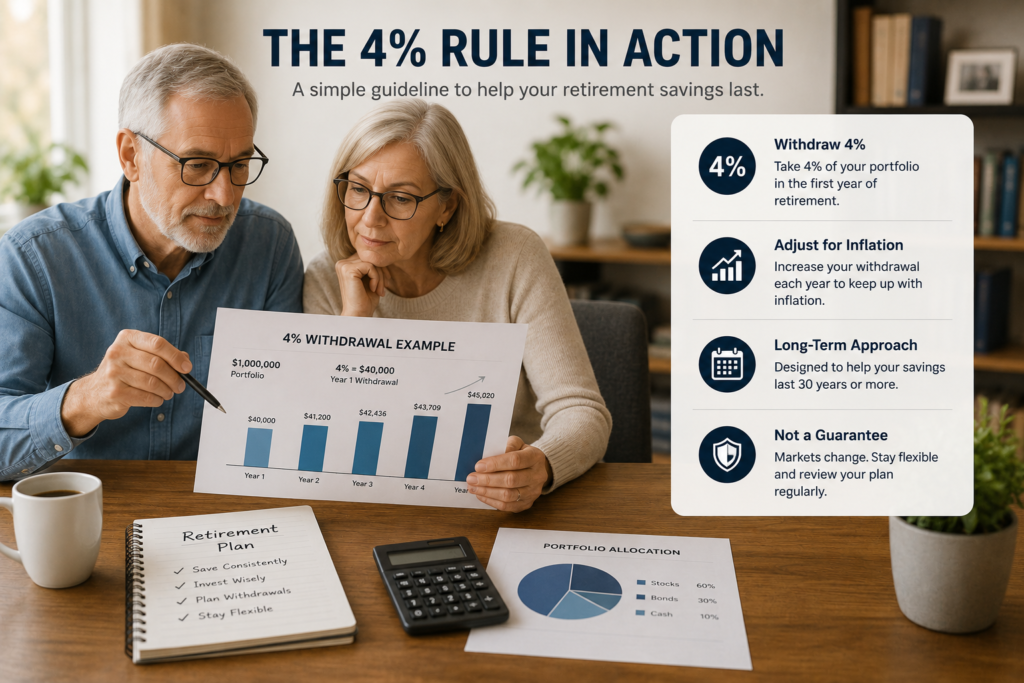

During your first year of retirement, you withdraw 4% of your investment portfolio.

After that, you adjust the amount each year to account for inflation rather than taking another fixed percentage.

For example, imagine you’ve saved $1 million.

Following the 4% rule, your first year’s withdrawal would be $40,000.

If inflation is 3% the following year, your withdrawal would increase to approximately $41,200, regardless of how the market performed that year.

The goal is to provide a steady income while giving your investments a reasonable chance of lasting for decades.

Where Did the Rule Come From?

The idea became widely known after financial planner William Bengen published research in the 1990s.

He analyzed decades of historical market data and found that retirees who withdrew around 4% from a diversified portfolio had a high probability of not running out of money over a 30-year retirement.

His research wasn’t trying to predict the future.

Instead, it looked at how different withdrawal rates would have performed under many historical market conditions.

That’s an important distinction that often gets overlooked.

Why People Still Use It

One reason the 4% rule has remained popular is its simplicity.

Retirement planning can quickly become overwhelming.

The rule provides a practical framework that helps people estimate how much savings they may need before leaving the workforce.

It also encourages long-term thinking instead of reacting emotionally to short-term market movements.

For many people, that’s valuable in itself.

Why Some Experts Question It Today

The world has changed considerably since the original research was published.

People are living longer.

Interest rates have gone through long periods of being unusually low.

Healthcare costs continue to rise in many countries.

Markets have also become increasingly global and, at times, more volatile.

Because of these changes, some financial planners believe a lower withdrawal rate—such as 3.5% or even 3%—may be more appropriate for retirees who expect very long retirements or prefer a larger margin of safety.

Others argue that flexible spending is more realistic than following one fixed percentage every year.

Flexibility May Matter More Than a Formula

One criticism of the 4% rule is that real life rarely follows a fixed plan.

Retirees don’t spend the exact same amount every year.

Travel expenses may be higher during the early years of retirement.

Healthcare costs often increase later in life.

Unexpected repairs, helping family members, or changes in the economy can all affect spending.

Rather than treating the 4% rule as a strict formula, many retirees use it as a reference point and adjust their withdrawals when circumstances change.

Your Retirement Is Different From Everyone Else’s

No retirement strategy works equally well for everyone.

Someone with a generous pension may withdraw very little from investments.

Another retiree may depend almost entirely on their investment portfolio.

Lifestyle, life expectancy, taxes, healthcare, and market performance all influence how much you can safely spend.

That’s why personal planning matters more than following any single rule.

Common Misunderstandings

Many people assume the 4% rule guarantees they will never run out of money.

It doesn’t.

Others believe it means withdrawing exactly 4% every year.

That’s not how the original research worked.

The rule adjusts withdrawals for inflation rather than recalculating a new percentage annually.

Understanding these details helps avoid unrealistic expectations.

Final Thoughts

The 4% rule has stood the test of time because it offers a simple way to begin thinking about retirement withdrawals.

Even after decades of discussion, it remains one of the most useful starting points available.

At the same time, retirement today looks different than it did thirty years ago.

Longer life expectancies, changing markets, inflation, and individual financial goals all deserve careful consideration.

Instead of asking whether the 4% rule is right or wrong, it may be more helpful to ask whether it fits your retirement plan.

For many people, the best strategy isn’t following one rule perfectly.

It’s staying flexible, reviewing your finances regularly, and adjusting your spending as life changes.

Frequently Asked Questions

Is the 4% rule still considered safe?

Many financial professionals still view it as a useful starting point, but some recommend lower withdrawal rates depending on market conditions and retirement length.

Does the 4% rule include Social Security?

No. The rule applies only to your investment portfolio. Income from pensions or Social Security is usually considered separately.

What happens if the market crashes?

One criticism of the rule is that large market declines early in retirement can increase the risk of running out of money. Some retirees respond by temporarily reducing withdrawals during difficult market periods.

Can I withdraw more than 4%?

Possibly. The right withdrawal rate depends on factors such as your age, other income sources, investment portfolio, and spending needs.

Continue Reading

The 4% rule helps answer how much you might withdraw each year, but another important question remains:

Where should those withdrawals come from first?

Should you spend cash before selling investments? Withdraw from taxable accounts before retirement accounts? Or take income from dividends instead?

Coming up next: The Best Order to Withdraw Retirement Income: A Simple Strategy That Can Make Your Savings Last Longer