Once retirees begin building an investment portfolio, one question comes up again and again:

Should I invest in bonds or dividend stocks?

It’s a reasonable question because both are often associated with retirement income. They can provide regular cash flow, help support everyday expenses, and play an important role in a long-term financial plan.

But despite those similarities, they’re very different investments.

Understanding what each one does—and where each one fits—can help you build a portfolio that’s better prepared for both good markets and difficult ones.

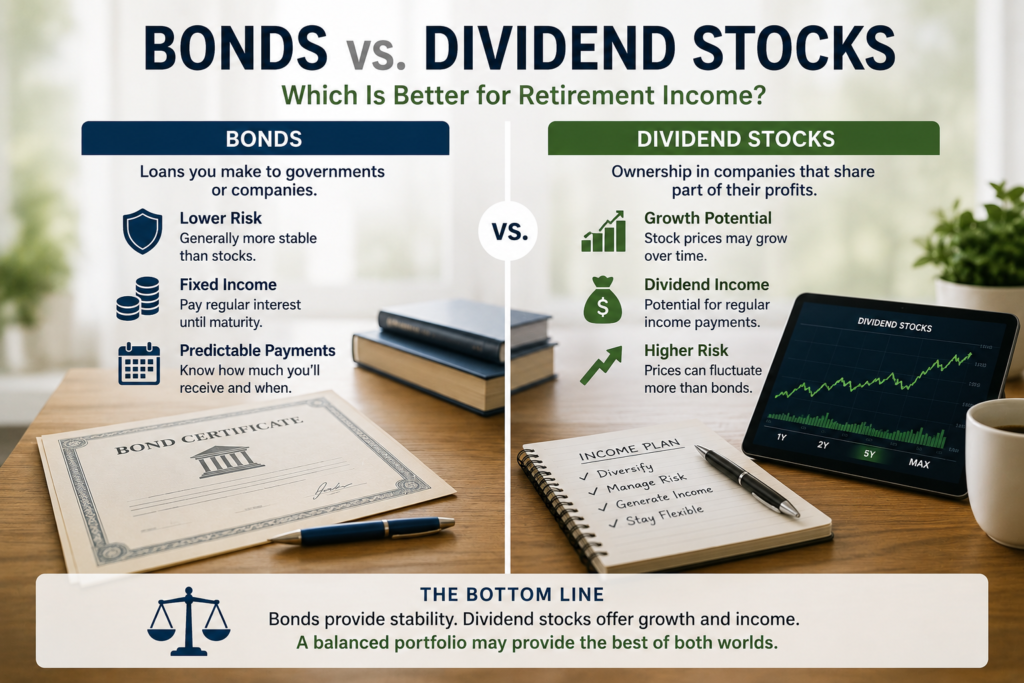

What Are Bonds?

A bond is essentially a loan.

When you buy a bond, you’re lending money to a government or a company. In return, they agree to pay you interest over a set period before eventually returning your original investment when the bond matures.

Many retirees appreciate bonds because they tend to fluctuate less than stocks.

That doesn’t mean they’re risk-free. Bond prices can still move as interest rates change, and there’s always the possibility that a borrower could fail to repay its debt.

Still, bonds are generally viewed as one of the more stable parts of a retirement portfolio.

What Are Dividend Stocks?

Dividend stocks are shares of companies that distribute part of their profits to shareholders.

Unlike bonds, dividend stocks represent ownership in a business.

That means your investment can grow if the company performs well, but its value can also fall during market downturns.

Some companies have built long histories of increasing their dividends year after year, making them attractive to investors looking for both income and long-term growth.

However, dividends are never guaranteed.

A company facing financial difficulties may reduce or even suspend dividend payments.

Stability vs. Growth

One of the biggest differences between bonds and dividend stocks is what they aim to provide.

Bonds generally prioritize stability and predictable income.

Dividend stocks offer the possibility of both income and capital appreciation, but they also come with greater price volatility.

For retirees who rely heavily on investment income, this trade-off is worth understanding.

Some investors are comfortable accepting market fluctuations in exchange for higher long-term growth potential.

Others prefer the relative stability that bonds can offer.

How Inflation Changes the Picture

Inflation affects every retirement plan.

While bonds may provide dependable interest payments, inflation can gradually reduce the purchasing power of that income over time.

Dividend-paying companies, on the other hand, sometimes increase their dividend payments as profits grow.

Although there’s no guarantee this will happen, dividend growth has the potential to help investors keep pace with rising living costs.

That’s one reason many retirement portfolios include both investments rather than choosing only one.

Many Retirees Use Both

The discussion isn’t always “bonds or dividend stocks.”

For many investors, it’s “how much of each?”

A balanced portfolio might include bonds to provide stability during uncertain markets, while dividend stocks contribute income and long-term growth potential.

The right mix depends on several factors, including:

- Your age

- Other retirement income sources

- Monthly expenses

- Investment experience

- Comfort with market fluctuations

There’s no universal allocation that works for everyone.

Questions Worth Asking Yourself

Instead of asking which investment is better, consider asking:

- Would a temporary market decline keep me awake at night?

- How much income do I actually need from my portfolio?

- Do I expect to use these investments for the next five years—or the next thirty?

- Am I investing mainly for stability, growth, or a combination of both?

Your answers often provide more useful guidance than comparing historical investment returns.

Common Mistakes

Many retirees make the mistake of moving entirely into bonds because they believe retirement means avoiding all stock market risk.

Others do the opposite, investing heavily in dividend stocks while underestimating how uncomfortable market downturns can feel once regular paychecks stop.

Both approaches can create unnecessary challenges.

Retirement investing isn’t about choosing one “perfect” investment.

It’s about combining different investments so they complement one another.

Final Thoughts

Bonds and dividend stocks each have strengths.

Bonds may provide stability and predictable income.

Dividend stocks offer the opportunity for growing income and long-term appreciation.

Neither investment is automatically better than the other.

The best retirement portfolios are often built around balance rather than extremes.

As your retirement progresses, your ideal mix may also change.

Regularly reviewing your portfolio can help ensure it continues supporting both your financial needs and your peace of mind.

Frequently Asked Questions

Are bonds safer than dividend stocks?

In general, bonds tend to experience less price volatility than stocks, although they still carry risks such as interest rate changes and credit risk.

Can retirees live on dividend income alone?

Some retirees do, but many combine dividend income with pensions, Social Security, bonds, and other investments to create a more diversified retirement income plan.

Should retirees own both bonds and dividend stocks?

Many financial professionals recommend holding a mix of investments because they serve different purposes within a retirement portfolio.

Which investment performs better during inflation?

Dividend stocks may have greater potential to increase income over time, while traditional fixed-income bonds can lose purchasing power if inflation remains high

Continue Reading

Now that you’ve seen how bonds and dividend stocks work together, the next step is understanding how much you can safely withdraw from your investments each year without running out of money.

Coming up next: The 4% Rule Explained: Does It Still Work for Today’s Retirees?